Hidden Costs of Owning Rental Property (12 Line Items)

The hidden costs of owning rental property are the line items that do not show up in your beginner pro-forma but show up on your bank statement. PITI (principal, interest, taxes, insurance) is the loud number. The 12 line items below are the quiet ones. Together they explain why a property that looks like it cashflows on Zillow's mortgage calculator can actually run negative for years.

This article is for first-time landlords (and aspiring landlords still in underwriting) who want their pro-forma to match reality. If you have plugged numbers into a spreadsheet and felt something was off, this list is the missing inputs. The honest answer is not "real estate is rigged." It is "the standard pro-forma is missing 12 line items, and adding them fixes the math."

Key Takeaways

- PITI is roughly half of what a rental actually costs. The other half is what beginner pro-formas usually skip.

- The 50% rule (operating expenses run about 50% of gross rent) is conservative for a reason. Most beginners underestimate, not overestimate.

- Capital expenditures (CapEx) are the single most-missed line item. Roofs, HVAC, water heaters, and windows have predictable lifespans and predictable costs.

- Property taxes often jump 15-30% on sale because of reassessment rules. Use the post-sale assessed value, not the seller's old tax bill.

Table of contents

- Why beginner pro-formas miss these costs

- The 12 hidden costs, with dollar ranges

- The 50% rule and why it works

- How to budget for unknowns

- FAQ

Why beginner pro-formas miss these costs

Before using this list, see how to calculate NOI on a rental property and how to calculate cap rate for the underwriting framework these line items belong inside.

The standard mortgage calculator is built for primary residences, where the question is "can I afford this monthly payment." Investment underwriting needs to answer a different question: "what is the net cashflow after all operating expenses, including the ones that happen every 7-15 years."

Most online calculators only show PITI plus management. That is not a rental pro-forma. That is a homeowner's payment estimate with a label change.

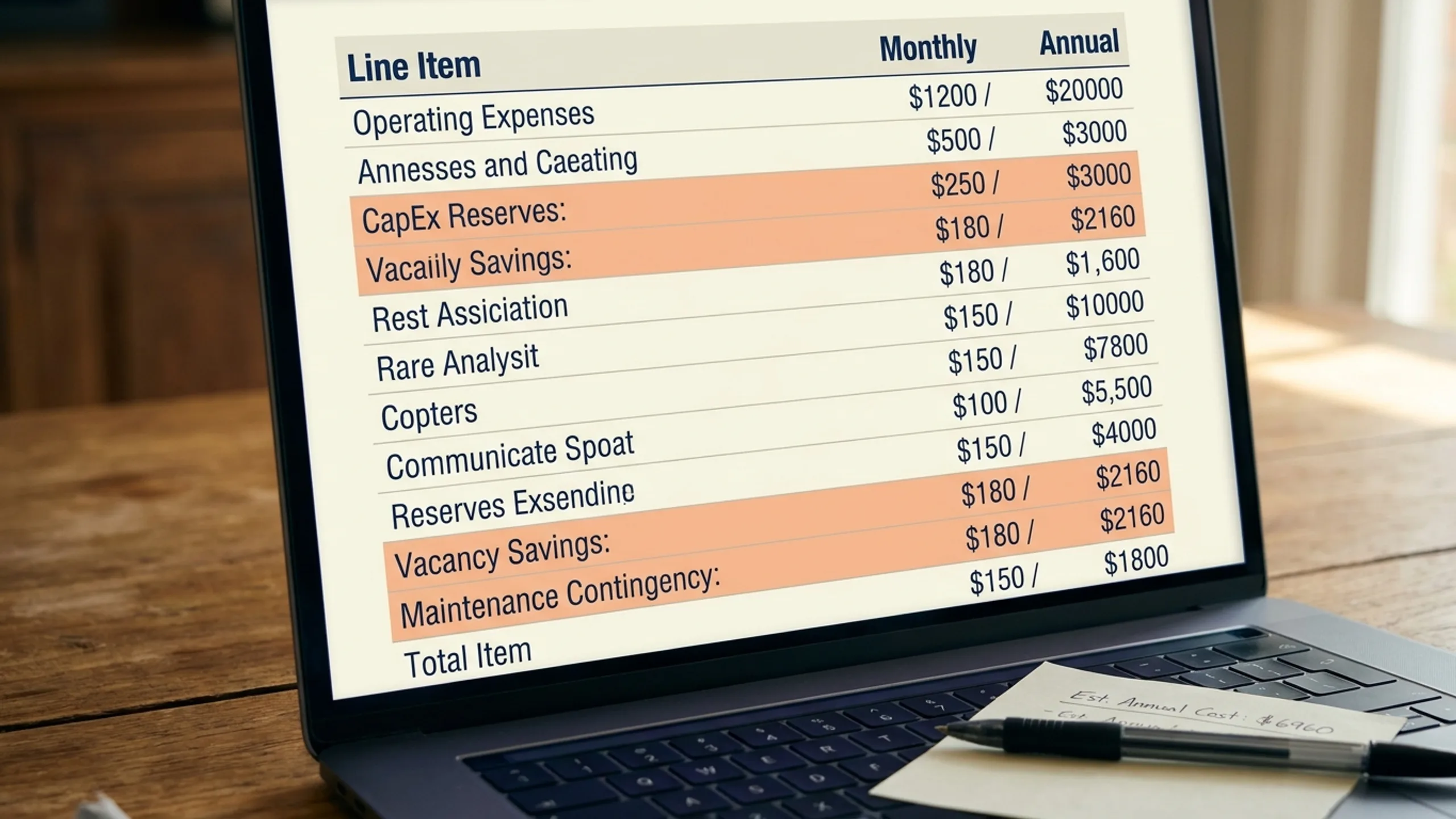

The 12 hidden costs

1. Capital expenditures (CapEx)

What it is: the cost of replacing major components when they wear out. Roof, HVAC, water heater, windows, kitchen appliances, flooring, exterior paint.

Typical cost: $300-$600 per month allocated, on a $200k-$300k property. Per the National Association of Home Builders cost-of-construction surveys, component lifespans run roughly: roof 20-25 years, HVAC 15-20 years, water heater 8-12 years, kitchen appliances 10-15 years, flooring 7-15 years.

The fix: allocate $200-$500/month per property to a CapEx reserve, depending on age and condition.

2. Vacancy

What it is: the time between tenants when no rent comes in.

Typical cost: 5-10% of gross annual rent. The U.S. Census Bureau Housing Vacancies and Homeownership survey shows the U.S. rental vacancy rate hovering between 6.0% and 7.5% over the past decade.

The fix: assume 8% vacancy in your underwriting unless you have specific data on your submarket.

3. Tenant turnover

What it is: when a tenant leaves, you pay for cleaning, paint, minor repairs, marketing, and screening for the next tenant. Even a smooth turnover costs $500-$2,000.

Typical cost: $500-$2,000 per turnover. Average tenant tenure on a single-family rental is 2-3 years.

The fix: assume one turnover every 24-30 months, budget $1,000-$1,500.

4. Property management

What it is: if you hire a property manager (and most long-distance investors should), they take 8-12% of monthly rent plus typically one month's rent for placement on every new tenant.

Typical cost: 8-12% of gross rent monthly + 50-100% of one month's rent per new tenant placement.

The fix: if you self-manage, you save the cost but pay it in time. Realistically value your time at $20-$50/hour and add it back to the pro-forma.

5. Insurance (landlord premium)

What it is: rental properties cost more to insure than primary residences. A landlord policy typically runs about 25% higher than a homeowner's policy on the same property.

Typical cost: $800-$2,500 per year for a single family rental. Insurance premiums in coastal Florida and California have increased 30-100% in some submarkets over the past 3 years per industry data.

The fix: get an actual quote on the specific property; do not estimate from the seller's bill.

6. Property tax reassessment

What it is: in most states, property taxes are reassessed when a property changes hands. The seller's old tax bill is not your tax bill.

Typical cost: sale price triggers reassessment in most U.S. counties. Your tax bill is usually based on a percentage of the post-sale assessed value, not the prior owner's lower assessment.

The fix: use a tax estimate based on the recent sale price. In California, Proposition 13 reassessment can mean your bill is 2-5x the prior owner's. In Texas, annual reassessment can push taxes up 8-10% per year.

7. Legal and eviction costs

What it is: lease drafting, lease updates, and (if needed) the cost of an eviction.

Typical cost: $200-$500 to have a lawyer review or draft a state-compliant lease. An eviction filing typically costs $250-$1,500 in court fees plus 1-3 months of unpaid rent and damages. Per state, eviction timelines run 2-12 weeks.

The fix: budget $300-$500/year baseline; assume one eviction every 5-10 years.

8. Bookkeeping and accounting

What it is: rental income and expenses get reported on Schedule E of your federal tax return. Per IRS Publication 527, every category of income and expense gets line-itemed annually.

Typical cost: $200-$600 per property per year for software (Stessa, Hemlane) plus tax preparation. A CPA familiar with real estate typically charges $300-$800 to file Schedule E annually.

The fix: budget $50-$100/month per property for accounting infrastructure.

9. Utilities during vacancy

What it is: when a property is empty between tenants, you pay water, electricity, gas, trash, and sometimes lawn or snow service.

Typical cost: $100-$400/month during vacancy.

The fix: budget for 4-6 weeks of utilities per turnover.

10. HOA dues and special assessments

What it is: condo and townhome HOAs charge monthly dues. They also occasionally charge special assessments (one-time levies for major repairs the HOA reserves do not cover).

Typical cost: $100-$700/month for HOA dues. Special assessments range from $500 to $20,000+ per occurrence.

The fix: read the HOA reserve study before buying. Underfunded HOAs (less than 70% reserve funding) signal future special assessments.

11. Lawn, snow, and seasonal services

What it is: in single family rentals, the landlord usually pays for lawn care between tenants and may pay for snow removal year-round.

Typical cost: $50-$200/month seasonal. Snow removal in northern climates can add $300-$1,500/year.

The fix: for single-family in cold climates, budget $1,000-$2,000/year for seasonal services.

12. Permits, inspections, and registration

What it is: many municipalities require landlord licenses, rental registration, and periodic inspections.

Typical cost: $50-$300/year per property, varying by city. New York, Philadelphia, Minneapolis, and many California cities have rental registration programs with fees and recurring inspections.

The fix: check the city or county housing department before buying. The annual cost is small but the legal exposure for unregistered rentals can be large.

The 50% rule and why it works

The 50% rule says: operating expenses (everything except mortgage principal and interest) typically run about 50% of gross rent on a stabilized rental. So if a property rents for $2,000/month, expect about $1,000/month in operating expenses (taxes, insurance, vacancy, maintenance, CapEx, management, utilities, legal, accounting, all of it).

The rule looks lazy. It is not. It is the empirical observation that the 12 line items above tend to add up to roughly half of gross rent across most U.S. markets. Some properties run cheaper (newer, no HOA, low-tax state); some run more expensive (older, cold climate, expensive HOA, high-tax state). 50% is the conservative starting point. See the 1% rule and the 50% rule explained for more.

If your detailed underwriting comes in significantly below 50%, you have probably skipped a line item. Re-check against the list above.

How to budget for unknowns

You cannot budget the unknown perfectly. You can hold reserves that absorb it.

- 6 months of PITI in cash as a baseline reserve.

- A separate CapEx fund that grows by $200-$500/month per property, used only for major component replacements.

- One full year of vacancy for special situations (uninhabitable property, eviction, market downturn).

Reserves are not optional. Reserves are the difference between a bad year and a forced sale. See how to calculate NOI on a rental property for the line-item model that produces the right reserve sizing.

Frequently Asked Questions

What is the biggest hidden cost of owning a rental property?

Capital expenditures (CapEx) is usually the largest under-budgeted line item. Roofs, HVAC systems, and water heaters wear out on predictable schedules but rarely show up in a beginner pro-forma. A $400/month CapEx allocation on a $200k property is normal; pro-formas that show $50/month "maintenance" and call it done are missing the structural costs.

How much should I budget for unexpected expenses on a rental property?

Most experts recommend 20-30% of monthly gross rent for unexpected expenses across maintenance, vacancy, turnover, and CapEx combined. On a $2,000/month rental, that is $400-$600/month in reserves on top of mortgage and taxes. Hold a separate cash reserve of at least 6 months of PITI for genuine emergencies.

Why do rental properties have higher property taxes than primary residences?

Many states tax rental property at a different rate than owner-occupied property, and most states reassess tax basis when a property is sold. The seller's old tax bill is rarely your new tax bill. Some states (California, Florida, others) have homestead exemptions that only apply to owner-occupied property; once it converts to a rental, the exemption disappears. Always estimate taxes from the post-sale assessed value.

Is property management worth the 10% fee?

If you live more than 30-60 minutes from the property, almost always yes. A good property manager handles tenant placement, maintenance coordination, rent collection, lease enforcement, and the legal exposure of self-managing under the Fair Housing Act. The 8-12% fee buys back your evenings and weekends, and it correctly classifies the rental as passive activity for tax purposes.

What is the 50% rule in real estate?

The 50% rule says non-mortgage operating expenses on a typical U.S. rental run about 50% of gross rent. If a property rents for $2,000/month, expect about $1,000/month in non-mortgage costs (vacancy, repairs, CapEx, taxes, insurance, management, accounting, etc.). The remaining $1,000 covers PITI and any cashflow. The rule is a sanity check; underwriting that comes in much below 50% has usually skipped line items.

Are landlord insurance premiums tax-deductible?

Yes. Per IRS Publication 527, landlord insurance premiums are fully deductible as an operating expense on Schedule E. The same applies to most operating costs (management fees, repairs, advertising, legal, accounting, mileage, and depreciation on the building). Keep clean records and a separate bank account so the deductions hold up under audit.

The 12 line items above are the gap between "this looks like it cashflows" and "this actually cashflows." Add them to your underwriting before you make an offer, not after the first surprise repair. The free 28-day course walks through the full line-item model in week 1.